Discover the 5 common mistakes in life insurance people make when buying life insurance. Learn what to avoid and protect your family’s future.

Table of Contents

Introduction – mistakes in life insurance

Life insurance is one of the most important financial tools you can have to protect your loved ones. Yet, despite its importance, many people fall into common traps when purchasing a policy. Some buy too little coverage, others believe in old insurance myths, and many don’t review their plans until it’s too late.

In this guide, we’ll break down 5 major mistakes in insurance that people often make when buying life insurance. By the end, you’ll understand what to avoid, how to make smarter decisions, and how to make sure your family’s financial security is never at risk.

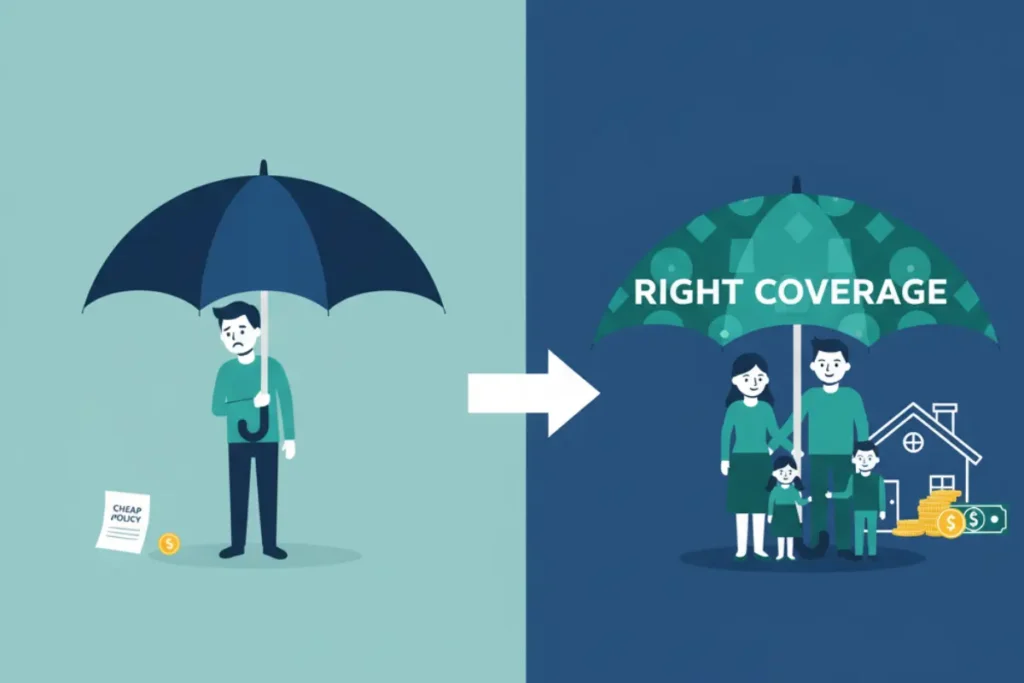

⚡ Quick Infographic: 5 Mistakes in Insurance

| Mistake | Impact | Fix |

|---|---|---|

| Believing myths | Delay & higher premiums | Check facts early |

| Choosing cheapest policy | Low coverage | Balance cost & benefits |

| Not updating policy | Outdated coverage | Review every 2-3 yrs |

| Skipping riders | Missed protection | Add key riders |

| Not comparing insurers | Pay more, get less | Compare 3+ quotes |

Mistake 1: Believing Insurance Myths Without Research

One of the most damaging mistakes in insurance is blindly believing insurance myths. These myths are often passed down by friends, family, or even social media, but they rarely reflect the truth.

Common insurance myths include:

- “I don’t need life insurance because I’m young and healthy.”

Reality: Life is unpredictable. Premiums are much cheaper when you’re young, so waiting can cost you more. - “Employer-provided life insurance is enough.”

Reality: Most employer policies cover only 1–2 times your annual salary, which is rarely enough for long-term family needs. - “Stay-at-home parents don’t need coverage.”

Reality: Their contribution to childcare and household management has real financial value that needs protection.

Pro tip: Always fact-check with a certified financial advisor or reliable sources like NAIC (National Association of Insurance Commissioners).

Mistake 2: Choosing the Cheapest Policy Without Considering Coverage

It’s tempting to go for the cheapest premium, but low cost often equals low coverage. Choosing based only on price is one of the biggest mistakes in insurance.

Why it’s risky:

- You may leave your family underinsured.

- Cheap policies might exclude important riders or benefits.

- Some policies adjust premiums over time, making them more expensive later.

Things to consider before buying:

- Coverage amount: Is it enough to pay off debts, cover children’s education, and maintain living standards?

- Policy type: Term insurance vs. whole life insurance — which suits your financial goals better?

- Long-term affordability: Can you sustain payments for the next 20–30 years?

Remember, life insurance isn’t just about saving money now — it’s about long-term protection.

Mistake 3: Not Reviewing and Updating Your Policy

Life changes, and so should your insurance. Yet, many people forget to review their policies after major life events.

When to update your policy:

- Marriage or divorce

- Birth of a child

- Buying a house with a mortgage

- Starting or selling a business

- Changes in health or income

Example: Imagine buying a policy 10 years ago when you were single. Now you’re married with two kids and a mortgage, but your coverage hasn’t changed. That old policy won’t provide enough protection for your family today.

Pro tip: Review your insurance at least once every 2–3 years or after any major milestone.

Mistake 4: Ignoring Riders and Add-Ons

Another mistake in insurance is overlooking policy riders, which can provide extra protection for a small additional cost.

Useful riders include:

- Critical illness rider: Covers serious health conditions like cancer or heart disease.

- Accidental death benefit rider: Pays extra if death is due to an accident.

- Waiver of premium rider: Waives future premiums if you become disabled and unable to work.

People often skip these add-ons because they don’t want to increase their premiums. But in many cases, riders are affordable and provide significant value.

Mistake 5: Not Comparing Multiple Insurance Options

Many people just go with the first policy offered by their agent or bank. But failing to compare is one of the most costly mistakes in insurance.

Why comparison matters:

- Premiums can vary significantly between companies.

- Some insurers offer better claim settlement ratios than others.

- Benefits and exclusions differ widely.

How to compare effectively:

- Use trusted comparison websites (like Policygenius)

- Check customer reviews and financial strength ratings

- Speak with independent advisors instead of just one company’s agent

By taking a little extra time to compare, you can save money and ensure better coverage.

Things to Avoid in Buying Insurance ( mistakes in life insurance )

To summarize, here are the top things to avoid in buying insurance:

- Believing common insurance myths without checking facts

- Choosing the cheapest policy only for price

- Forgetting to update policies after life changes

- Ignoring valuable riders and add-ons

- Not comparing multiple insurers before deciding

Avoiding these mistakes in insurance will help you make smarter decisions and safeguard your family’s future.

| # | Mistake | What it looks like / Why it’s harmful | How to avoid |

|---|---|---|---|

| Choosing based on price only | Buying the cheapest policy without checking coverage, exclusions, or insurer reputation — can leave loved ones underprotected when a claim is needed. | Compare features (sum assured, riders, exclusions) and insurer claim-settlement record — not just premium. Use quotes from multiple insurers. | |

| Buying the wrong type of policy | Picking a short-term or investment-focused plan when you need long-term income protection — may leave gaps in financial security. | Identify your primary goal (income protection, investment, tax planning) and choose term, endowment, or ULIP accordingly. Prioritize pure term for protection. | |

| Underestimating required coverage | Calculating a low sum assured (e.g., only a few years of income) ignores inflation, debts, children’s education and future needs — beneficiaries may struggle financially. | Use a needs-based approach: cover outstanding debts, living expenses for dependents (5–15 years), future goals (education, marriage) and an inflation buffer. | |

| Ignoring policy fine print & exclusions | Missing exclusions (suicide clause, pre-existing conditions, waiting periods) or ambiguous terms can lead to rejected claims or reduced payout. | Read policy documents carefully (benefits, waiting periods, exclusions). Ask the agent or insurer for written clarification on any unclear clause before signing. | |

| Not reviewing/updating the policy | Life changes — marriage, children, home loan, income changes — can make an old policy inadequate. Leaving it unchanged may expose gaps later. | Review your policy every 2–3 years or after major life events. Increase sum assured or add riders (critical illness, waiver of premium) as needed. |

FAQs

What are the biggest mistakes people make when buying life insurance?

The most common mistakes include buying too little coverage, believing insurance myths, ignoring policy updates, skipping riders, and not comparing providers.

How do I know if I have enough life insurance coverage?

A general rule of thumb is 10–15 times your annual income, but it also depends on debts, dependents, and lifestyle needs.

Can I change my insurance policy later?

Yes, most policies allow you to adjust coverage or add riders. However, premiums may increase if your health has changed.

Is term insurance better than whole life insurance?

Term insurance is usually cheaper and ideal for pure protection, while whole life offers savings and investment benefits. The best choice depends on your goals.

Conclusion

Life insurance is not just a contract; it’s a promise to your loved ones. Falling for insurance myths, choosing the cheapest policy, or not reviewing coverage are mistakes that can cost your family dearly in the future.

When buying life insurance, always compare, review, and customize your policy. By avoiding these mistakes in insurance, you’ll ensure that your family remains financially secure no matter what happens.

👉 Call to Action: Take a few minutes today to review your current policy or explore new options. Protect your family’s tomorrow by making the right choice today.

Internal Linking Suggestions:

- Link to an article about “Term vs Whole Life Insurance”

- Link to a guide on “How to Calculate the Right Life Insurance Coverage”

External Linking Suggestions:

Hi, I’m Sandip Bhange, the person behind MyFinancePolicy. I’m a civil engineer who developed a strong interest in banking and personal finance over the years. I started this website to share clear, honest, and easy-to-understand information that can actually help people in their daily financial decisions.